Bitcoinpolitisk Institutt, or Bitcoin Policy Norway, organized a neat panel session at its events in Oslo’s Litteraturhuset last week. The Satoshi-samtale (“Satoshi talks”) is recorded and released as a podcast, worth listening for a deep dive into the monetary economics of Bitcoin.

For years, BPI has put on semi-regular events in Oslo and this one doesn’t disappoint. Two guests from the banking system (Jan Ludvig Andreassen, the chief economist at Eika, and Arne Kloster, special adviser to Norges Bank) provided their views, with BPI’s Ole Emil Augland offering critical and, occasionally, quite critical, Bitcoin-oriented commentary.

Across topics that included the intricacies of the consumer price index, how inflation works through the economy, and how it relates to money printing, the panelists meandered toward what the point and purpose of a monetary system is. At the end, Arne gave us the most succinct conflict of visions involved between bitcoin and fiat:

“There’s a trade-off between stability and flexibility, and the monetary system we have today is very flexible but it comes with some risks, whereas a monetary system that’s closer to the old-fashioned gold standard is more stable but won’t perhaps contribute to economic growth in the same way.”

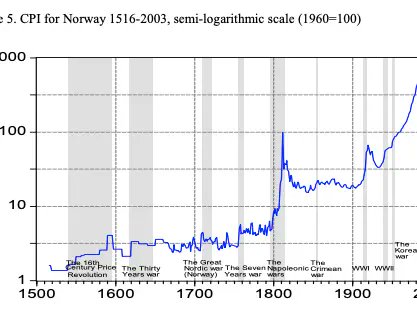

Here’s the consumer price index graph that Arne presented, based on research and statistics from Norges Bank, and which provided backdrop to the overall conversation:

Briefly going through that history, Arne suggests that “inflation is, in a way, a phenomenon of war; it’s when lots of money is printed to finance soldiers’ pay, food, canons… war is expensive.”

And what he brought to weigh on the subject was a very standard remark among the economics profession: What can be even worse than inflation is the price level change variability, “because that makes economic planning difficult.” Stable inflation is manageable since you know that the purchasing power of your money will fall by a particular, credible amount (i.e., the 2% creed), but when the change in money’s worth is unpredictable, money quickly loses its coordinating role and the monetary system turns into chaos.

Jan Ludvig interjected that household wealth has transformed greatly in the last four decades in Norway, where real estate is concerned. It used to be mostly owned by institutions, but from around 1985 Norway experienced “a historic transfer of value from institutions to households, which also meant that changes in property prices meant so much more than they used to. But they’re not part of the money supply!” Which they probably should, Jan Ludvig suggested.

In a beautifully phrased remark by Ole, about the downsides of calculating a consumer price index, we learn that just because a computer improved in raw, objective power (e.g., RAM, memory, speed), statisticians make an error in assuming that the economic value of the item has increased in proportion.

“They can’t say that ‘yes, the price should be 12,000 instead of 11,000 […] they’re trying to calculate objectively something that is subjective, that is value.”

You can learn more about Bitcoin Policy Norway (“Bitcoinpolitisk Institutt Norge”) and their work via BPINorge.no.